🔎 Value of Tax Shield with Permanent Debt

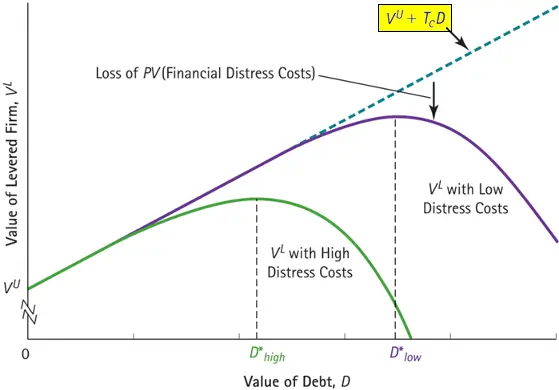

In the dotted line of the following diagram, Bruce sets the value of the tax shield equal to TCD:

Similarly, in sections, I encourage students to use the following formula:

- Present Value of the Interest Tax Shield of Permanent Debt =

The textbook has a nice explanation of the formula in section 16.3, which I reproduce for you here:

-

Rather than attempting to account for all possibilities here, we will consider the special case in which the firm issues debt and plans to keep the dollar amount of debt constant forever.

-

For example, the firm might issue a perpetual consol bond, making only interest payments but never repaying the principal. More realistically, suppose the firm issues short-term debt such as a five-year coupon bond. When the principal is due, the firm raises the money needed to pay it by issuing new debt. In this way, the firm never pays off the principal but simply refinances it whenever it comes due. In this situation, the debt is effectively permanent.

-

Many large firms have a policy of maintaining a certain amount of debt on their balance sheets. As old bonds and loans mature, they start new loans and issue new bonds. Note that we are considering the value of the interest tax shield with a fixed dollar amount of outstanding debt, rather than an amount that changes with the size of the firm.

-

As we learned in Chapter 6, if the debt is fairly priced, the Valuation Principle implies that the market value of the debt today must equal the present value of the future interest payments:

- Market Value of Debt D = PV (Future Interest Payments) (16.6)

-

Note: Equation 16.6 is valid even if interest rates fluctuate and the debt is risky, as long as any new debt is fairly priced. It requires only that the firm never repay the principal on the debt (it either refinances or defaults on the principal).

-

If the firm’s marginal tax rate (Tc) is constant, then we have the following general formula:

- Value of the Interest Tax Shield of Permanent Debt

- = PV (Interest Tax Shield)

- = PV (Tc× Future Interest Payments)

- = Tc× PV (Future Interest Payments)

- = Tc× D (16.7)

-

This formula shows the magnitude of the interest tax shield. Given a 25% corporate tax rate, it implies that for every $1 in new permanent debt that the firm issues, the value of the firm increases by $0.25.

Feedback? Email robmgmte2700@gmail.com 📧. Be sure to mention the page you are responding to.