🙋 Student Q&A (Lecture 6)

Click here to learn about timestamps and my process for answering questions. Section agendas can be found here. Email office hour questions to robmgmte2700@gmail.com. PS1Q2=“Question 2 of Problem Set 1”

📅 Questions covered Saturday, Mar 7

Section titled “📅 Questions covered , Mar 7”🕣 2:44pm

❔ Tornado diagrams for sensitivity analysis

✔ Covered earlier

🕣 2:45pm

❔ Exam review

✔ Covered earlier

🕣 2:45pm

❔ I just wanted to clarify one point regarding the upcoming Corporate Finance (MGMT E-2700) midterm exam. Since the exam is open book and open notes, I wanted to confirm whether it is permitted to access the problem set solutions on Pearson during the exam for reference, in the same way we might consult our notes or problem sets.

I just want to ensure I fully understand which resources are allowed so that I remain within the academic integrity guidelines.

Also, I was wondering if you plan to use the upcoming section as a review of the midterm material?

✔ You are allowed to do it, but you definitely shouldn’t be doing it because it will take too long. It’s vitally important that you have those skills in your head, because you just won’t have time to look things up in the problem sets. It’s just not feasible. You have to redo the problem sets until you know all of those skills, and at worst you’re going to be looking up a formula in the formula sheet. That would be my heartfelt advice, but if you’re just asking about policy, it’s not cheating, so you’re more than welcome to do it.

We did do a review today.

🕣 2:47pm

❔ I’m reaching out because I don’t quite understand a specific concept and was wondering if you could clarify it for me. What does the following mean: “Every company is a collection of assets and those assets can generate cash flows in the future. The value of the firm is the NPV of those cash flows.”?

✔ on video

🕣

❔ Could you please clarify why cash is subtracted when calculating Enterprise Value? Additionally, I am interested to know how the valuation is impacted in a scenario where a company’s total debt is less than its available cash.

✔ Cash is subtracted from Enterprise Value because if you were considering purchasing the stock and the bonds of a firm, you could borrow money to buy all of the stocks and the bonds of the firm. You could then use the firm’s own cash after you own the firm to pay back your debts. You can essentially use the cash of the firm to pay for the firm, which is why, when a private equity firm is thinking about Enterprise Value, they like the idea of subtracting off the cash. However, as your previous question indicated there is another way of thinking about why you subtract off cash, which is that if you’re using the market value of the stocks and the market value of the bonds to estimate how much the company is worth, part of that value will come from the company’s own cash hoard. However, if you want to know only what was referenced in your previous question, i.e., only about the collection of assets that are generating cash flows, that’s separate from the cash hoard.

If you want to think about the company as an enterprise, which has assets that generate cash flows, that’s separate from the cash flow, so just subtract that off. That’s a much harder way of thinking about it that I wouldn’t worry about for right now, but that’s another way to think about enterprise value that I think is more relevant for this class. Right now we’re preparing for the midterms, so I wouldn’t stress it.

🕣

❔ Could we go over what happened on the site? I multiplied 1/242.2 by each

side, but I do not understand why we are doing it this way.

Regarding the equation to connect them: Market-to-Book ratio = Share Price / Book Value per Share

I have tried to plug the numbers into the equation and solve it, but I would appreciate some clarification as I “chug” along to get the answer.

✔

🕣 2:55pm

❔

- Since Net Working Capital (NWC) involves current assets and liabilities, does this mean that Accounts Receivable and Accounts Payable are always assumed to be settled in less than a year? Furthermore, how is this timeframe determined? Should I be looking for specific indicators to know for certain, or is it standard practice to simply assume they fall within a one-year period?

✔ Part of the definition of AP and AR is that they are current asset/liabilities. That means that they will be settled within the current accounting period.

🕣

❔ 2. Also you could please walk me through the following topic, as I am having some difficulty understanding it: Payback Period when you must prorate.

While questions like the one below are fairly straightforward:

T: 0 | CF: -10 T: 1 | CF: 4 T: 2 | CF: 3 T: 3 | CF: 3 T: 4 | CF: 2

- I am struggling with scenarios where you don’t get paid back exactly on a year boundary. Could you please explain how to calculate the payback period for these cash flows? T: 0 | CF: -10 T: 1 | CF: 4 T: 2 | CF: 3 T: 3 | CF: 5 T: 4 | CF: 2

✔ After the first year, you’ve been paid back 4M. AFter the second year, you’ve been paid back 4+3=7M. After the third year, you are paid back 4+3+5=12M.

In the third year, you were paid back 5M total, but you only needed to be paid back 3M (=10-7). Therefore, it won’t take the full year, it will take 3/5.

Basically, you divide the amount of money you need by the total amount of money you get in the year.

📅 Questions covered Monday, Mar 9

Section titled “📅 Questions covered , Mar 9”🕣 7:42

❔ Is PS 4 available for practice yet?

✔ Tomorrow morning.

🕣 7:43pm

❔ Can you go over questions 13 or 14 in PS 3 in the next section,please?

✔

🕣 7:50pm

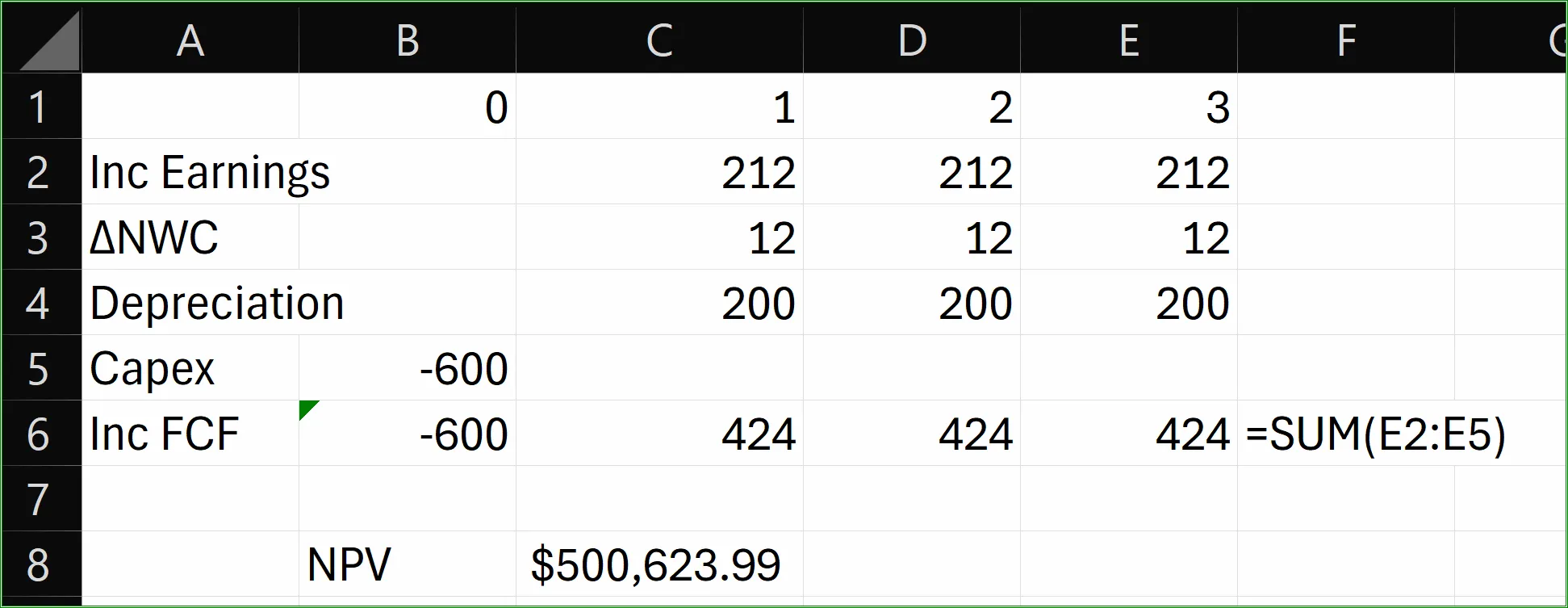

❔ I am trying to understand the logic behind receiving rent between T=1 and T=2, specifically why the first rental income cash flow is booked at T=2. I understand this is based on the conservative assumption that income accruing throughout the year is booked at the end of the year to allow for potential delays in collection, but I would appreciate a more detailed explanation to ensure I have a full grasp of the timing.

✔

🕣 7:53

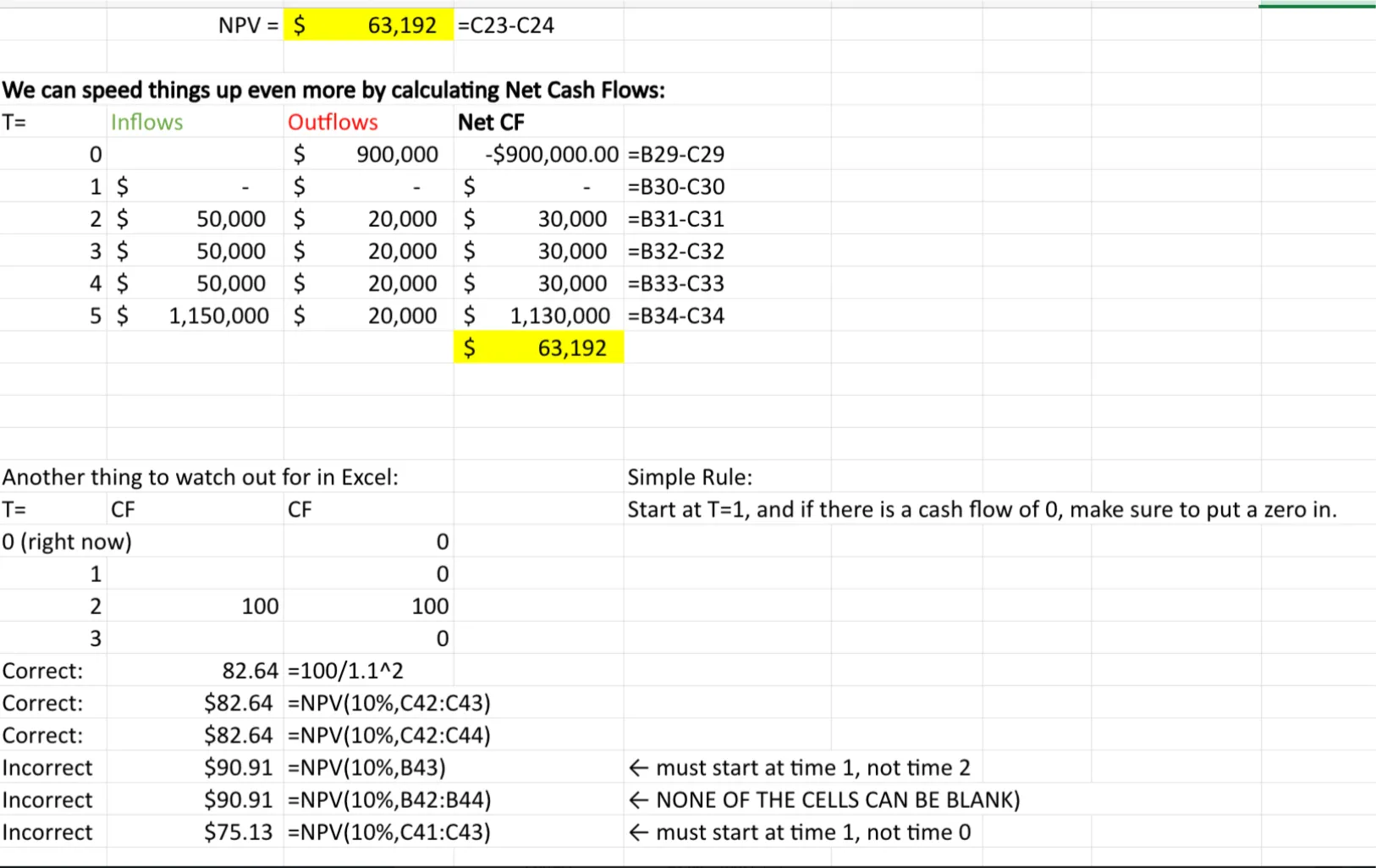

❔ I am writing to follow up on the image you shared. I feel like I need the image broken down a bit slower to fully understand the details.

Could you please provide a more step-by-step breakdown when you have a moment?

✔

🕣

❔ I have a question regarding a specific scenario I am reviewing. The scenario involves a manufacturer investigating how an increase in the cost of raw materials will impact the cost of manufacturing, the selling price, the quantity sold, and the project’s net present value (NPV).

Given that one change is creating a “domino effect” across several variables, I am trying to determine what type of analysis the manager is performing in this instance. Could you please clarify which type of analysis best describes this process?

✔ Scenario analysis (as opposed to sensitivity analysis) can involve a domino effect like what you describe. The way to distinguish between scenario and sensitivity analysis is whether several quantitative inputs to the model change simultaneously.

For example, if you are simultaneously changing price and quantity, it is scenario analysis. It can’t be sensitivity analysis because two of the quantitative variables that you use as raw inputs to the FCF modeling are changing.

Likewise, if you are simultaneously changing cost of goods sold and quantity, it is scenario analysis. It can’t be sensitivity analysis because two of the quantitative variables that you use as raw inputs to the FCF modeling are changing.

Basically, if you ever change two of the quantitative inputs to your model, it is scenario analysis. EVEN IF you are modeling your scenario on a specific other quantitative change. For example, suppose you are considering a scenario in which the average temperature rises. If the average temperature rising causes you to simultaneously changing price and quantity or simultaneously changing cost of goods sold and quantity, or change any other collection of multiple variables simultaneously, then it is scenario analysis.

🕣 8:00pm

❔ Could we go over the differences between sensitivity analysis and scenario analysis? I am specifically interested in understanding what tells them apart based on a real-life example.

✔

📅 Questions covered Tuesday, Mar 10

Section titled “📅 Questions covered Tuesday, Mar 10”No questions emailed.

📅 Questions covered Saturday, Mar 21 ✅

Section titled “📅 Questions covered , Mar 21 ✅”No questions emailed.

📅 No Section on Monday, Mar 24 ✅

Section titled “📅 No Section on , Mar 24 ✅”No section today. For more information, see the announcement on Canvas.

Feedback? Email robmgmte2700@gmail.com 📧. Be sure to mention the page you are responding to.