🙋 Student Q&A (Lecture 12)

Click here to learn about timestamps and my process for answering questions. Section agendas can be found here. Email office hour questions to robmgmte2700@gmail.com. PS1Q2=“Question 2 of Problem Set 1”

📅 Questions covered Saturday, May 2

Section titled “📅 Questions covered , May 2”🕣 1:59pm

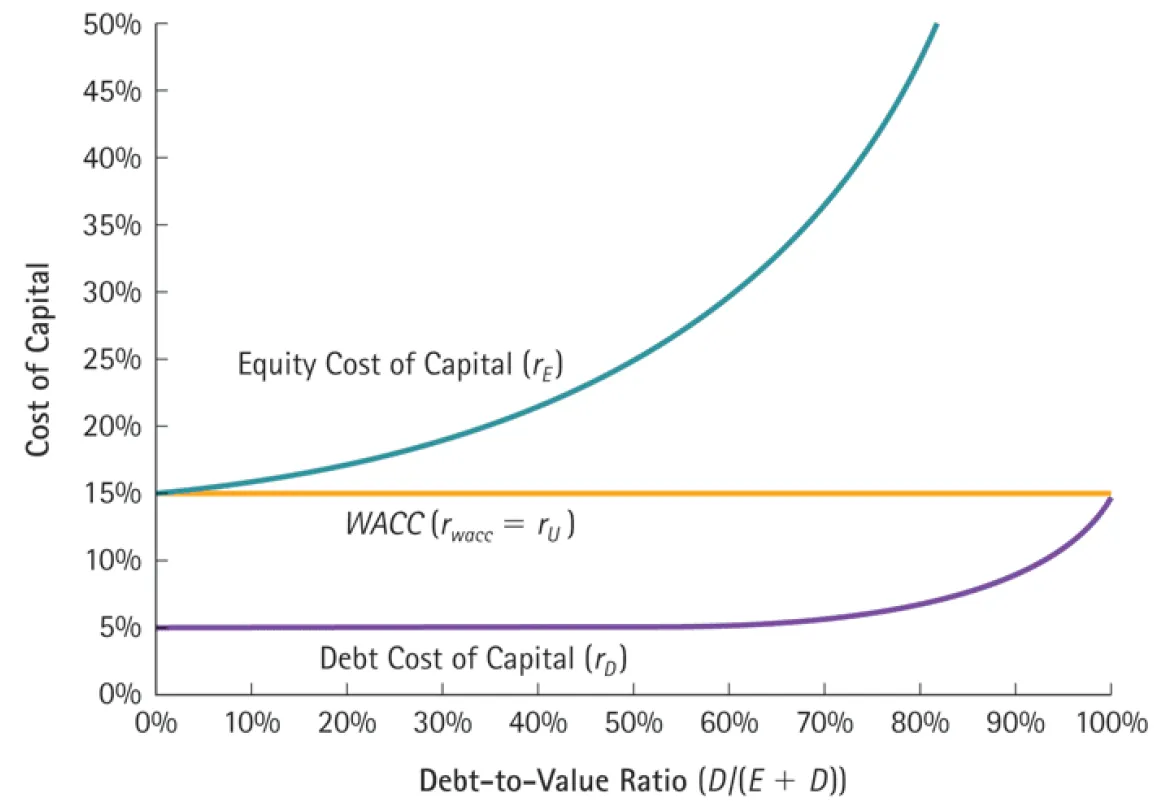

❔ I really enjoy the discussions on capital structure, which may be one of my favorite finance topics. I watched the video where you reviewed my spreadsheet on MMI & II (thank you), and have a follow-up question on the following graph (Slide 39 from Module 10 or April 14th):

If at D/(E+D) = 100% and Kd converges to WACC (Ru), wouldn’t the cost of equity (Ke) rollover to 0%? However, mathematically, if I plug the variables into the cost of equity of formula (Ke = 15% + 1/0(15%-15%)) I end up at an impasse because the D/E would be 1/0? What does this mean since you can’t divide an integer by 0?

✔

🕣 2:05pm

❔ I’m reviewing the slides today and I think Bruce mentioned in class that it may not be possible to have an IRR when the cash flow stream flips back and forth between positive and negative, but isn’t this the XIRR function in excel?

✔ It’s true that sometimes there is no IRR, and that sometimes there will be multiple IRRs.

Generally, multiple IRRs are due to the sign of the cash flows flipping too much as you described. Nonexistence of IRRs generally occurs in situations where an interest rate wouldn’t make sense. For example, if all of the cash flows are positive or all of the cash flows are negative, there won’t be an IRR.

My understanding is that XIRR uses numerical method to find an IRR (ie an interest rate (i) that makes the net present value (NPV) equal to zero). This means it starts with an initial guess (for example, i = 10%). It then adjusts i in the direction that gets the NPV closer to zero. In other words, if NPV is positive, it adjusts i very slightly to make NPV lower. If NPV is negative, it adjusts i slightly in the direction that makes NPV higher.

It then repeats this process many times until the value of i until NPV gets very close to zero.

Numerical methods like this omit thinking from the overall process, so they will not recognize when there are multiple solutions and will return the first value of i that makes NPV equal to zero. This is the danger of relying to heavily on software.

If the IRR doesn’t exist, it will keep trying different values of i but will never get the NPV close to zero. After 100 repetitions of the cycle described above, it will give up and return the value #num, which tells the user that it failed to find an answer.

📅 Questions covered Sunday, May 3

Section titled “📅 Questions covered Sunday, May 3”We covered the following questions:

- PS5 2, 3(last part), 7(b)

- PS6 1(last), 3, 10

🕣

❔ You work for a company with a dividend of $3 and a stock price of $40. The dividend is expected to grow at 2% per year on average. What is your cost of capital. (What is the return that you paying your stockholders)

✔ r_e = $3/$40 + 2% = 9.5%

🕣

❔ Suppose that the CAPM estimates that your return on equity is 11%. What would you expected dividend growth rate have to be for the Constant Dividend Growth Model to predict the same cost of equity?

✔ r_e = $3/$40 + growth = CAPMre = 11.5%

$3/$40 + growth = 11.5%

growth = 11.5% - 7.5% = 4%

📅 Questions covered Monday, May 4 NOON

Section titled “📅 Questions covered , May 4 NOON”🕣 12:52pm

❔ Mathematically, if a firm’s share price (post merger) is expressed as [(A+T+S)/(Proforma Shares)] and compared to [A/Original Shares] to see if intrinsic value has been added or destroyed, then technically (or theoretically) the only way the firm’s proforma price can be increased or decreased (or shareholders are better or worse off) is if there are synergies (S) or indirect costs (-S) present in the combination (assuming NO premiums or discounts)? However, if I now factor premiums and discounts into the equation, the value of numerator (A+T+S) stays the same, but the denominator adjusts the exchange ratio accordingly (Na + X) with X equal to target’s shares X the exchange ratio and target’s price reflects the premium or discount in the ratio. Interestingly, and assuming no synergies, the value of the firm does not change, but the composition of the value of the acquirer and target do depending on the premium (target’s price appreciates) or discount (acquirer’s proforma price higher) paid. Am I thinking about this correctly?

Furthermore, and although proforma EPS will increase, decrease, or remain the same depending on a merger, this reflects accretion or dilution, but technically does not change the value of the firm. To me, this concept appears to deviate from overpaying or underpaying for a company, am I on the right track here? Practically speaking, I find it hard to believe that if a deal is wildly accretive that the value in real life would not appreciate.

✔ See video.

Feedback? Email robmgmte2700@gmail.com 📧. Be sure to mention the page you are responding to.