🔎 What is Enterprise Value?

Market Cap tells us the value of the firm’s equity shares. But how do we value the firm, itself, as an “enterprise?” (By enterprise, we mean an ongoing business endeavor - a group of people and assets working together to generate cash flows.)

In this class, we will think of any enterprise as a collection of assets. Physical assets, human assets, and IP assets, etc. Therefore, we can rephrase the question as “How do we value the underlying business assets of a firm?”

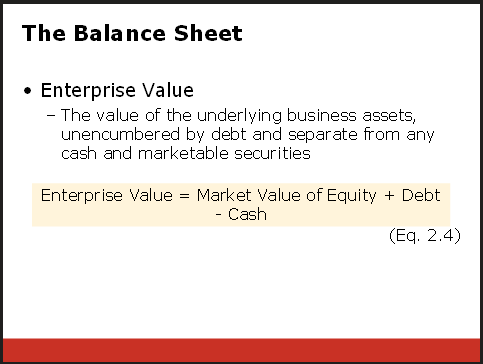

This is the question that Enterprise Value (EV) attempts to answer. It attempts to find “The value of the underlying business assets, unencumbered by debt and separate from any cash and marketable securities”

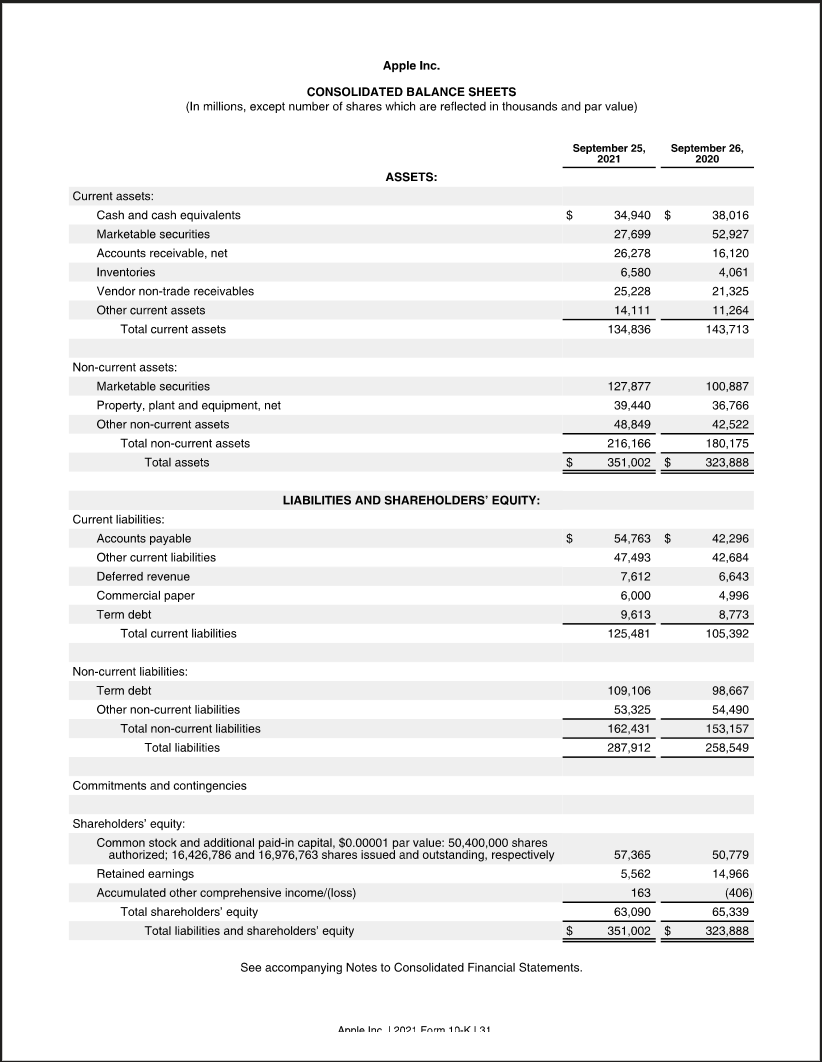

To understand how to do this, it will be helpful to look at a firm. Let’s look at Apple and let’s start with its accounting data. Here is a simplified version of Apple’s consolidated balance sheet from their 2021 10K (the full version is below - consolidated means that it incorporates the balance sheets of subsidiaries)

| Assets | Liabilities & Equity |

|---|---|

| $35B Cash $316B Other Assets | $125B Debt $163B Other Liabilities |

| $63B Shareholder Equity |

According to this, Apple’s assets are worth 35+316=$351B.

But is this true? Is Apple really only a $351B company?

EV is like Market Cap, but it takes debt and cash into account.

The total market value of a firm’s equity and debt, less the value of its cash and marketable securities. It measures the value of the firm’s underlying business.

This is a simple formula, but what does it mean? What is the intuition?

There are two ways of understanding this formula.

The easy way is the viewpoint of an acquirer.

The harder way is the viewpoint of corporate finance. This way may help you appreciate some differences in how financial ratios are interpreted.

The easy way: (the LBO approach to EV)

Enterprise Value is how much it would cost to purchase all claims on a company’s earnings. You buy out the owners and the creditors. You can use the cash holdings of the company to do this.

| EV = | Market Cap + | Debt - | Cash |

|---|---|---|---|

↑ cost to buy out owners P*#SharesOutstanding | ↑cost to buy out debt | ↑ you can use the company’s cash to pay down the debt. |

Does that work regardless of whether Market Cap is above or below Book Value?

Yes.

The hard way:

This is how you want to start thinking about it in this class. This way may help you appreciate some differences in how financial ratios are interpreted.

Every company is a collection of assets and those assets can generate cash flows in the future. The value of the firm is the NPV of those cash flows.

We trust market measures of value. So how does the market value this enterprise?

(by enterprise, we mean the assets and the cash flows they generate.)

The way that the market measures the value of this enterprise starts with market cap.

Of course MC isn’t the full story. To own the company, you must pay off the debt. So the value of the enterprise is “Market Cap + Debt.”

Finally, the cash a company may hold is not part of the true enterprise, so you can subtract it off.

The true Enterprise Value = Value of Assets = Market Cap + Debt - Cash

I investigated one time and found four different definitions of ROA.

Net Income/Assets EBIT/Assets (Net Income + Interest Expense (1-T) )/Assets

🙋♂️ What do we mean by “enencumbered” mean. It seems like the Enterprise Value formula actually adds in the debt.

Why do we even need a measure of the value of a firm’s underlying business assets?

There are a number of ways that Enterprise Value can be used. One way is to compare a firm to other firm’s by looking at its EBITDA in comparison to its Enterprise Value.

Just as we can compare stock price to earnings, we can also compare EBITDA to Enterprise Value.

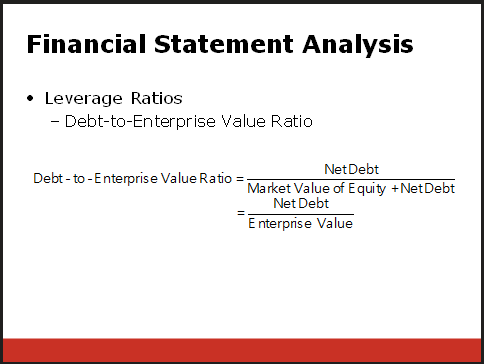

Likewise, it is more meaningful to compare debt to enterprise value than it is to compare it to market cap:

The reason I like this is that it approximates and improves on the following ratio as a way of measuring leverage:

Math note EV = MC + (Debt - Cash) = MC + (Net Debt) AAPL MC = 2760 Debt = 6+10+109=125 (We used the balance sheet historical cost value of the debt to approximate the market value of debt because market value of debt is hard to come by (bond markets are OTC). Cash = 35 EV = Market Cap + Market Value of Debt - Cash

First, the value of the enterprise is easily measured by the market cap.

However, the market cap is the value of the stock. But the stockholder’s are the only people who “have a piece of” the enterprise. In other words, there are other claims on the enterprise that must be paid off even before the stockholders. Specifically: debt. Therefore, if we really want to understand how much the ENTIRE enterprise is worth, we must add up both how much it’s worth the stockholders AND how much it’s worth the creditors.

Market Cap is how we estimate the value of the underlying business assets. However, it is encumbered by debt, because debt must be paid first before it can be distributed to stockholders. To get the value of the assets, “unencumbered by debt,” we add the MV of debt back in.

For example, the market data suggests that AAPL is worth 2760+125=2885 . The stock is only worth 2885-125=2760, because the stock is encumbered by debt.

What we have found so far when we calculate MC + Debt is the “value of the underlying business assets, unencumbered by debt.”

Enterprise Value = The value of the underlying business assets (unencumbered by debt) and separate from any cash and marketable securities

Part of the value of AAPL (as a whole, it’s worth 2885) comes from the fact that it has 35 billion of cash. In fact, we would say that $35B of AAPL’s 2.885T value comes from its .035T of cash. We subtract that off, because EV is meant to be a measure of the value of AAPL as “the company that makes iPhones and will be making it’s investors rich based on that franchise.” The actual money making machine that AAPL is is worth only 2885-35=2850. That’s its enterprise value.

Apple is worth 2850 from its enterprise and 35B from its cash, for a total of 2885B.