👨🏫 Notes

Notes:

- Sole Proprietorship - Doing business in your own name. The smallest companies.

- Partnership - A classic partnership.

- C Corporation - The classic corporation. Taxes: on dividends (and capital gains when you sell the stock).

- Limited Partnership - Great for hedge funds. In a hedge fund, general Partners manage the money of the Limited Partners. GPs are on the hook for the firm’s debts!

- Limited Liability Company (LLC) - Great for professional practices. Owners manage the firm, but they are not responsible for the firm’s debts if it is sued, so their assets are shielded.

- S Corporation - Has tax advantages over classic C-Corp, but makes your taxes more complex. The firm’s profits, etc. go directly on you personal tax forms, like with the partnerships, above.

| # of owners | Limited Liability/ Liability for Firm’s Debts | Owners Manage the Firm? | Ownership changes dissolve firm? | Taxation | |

|---|---|---|---|---|---|

| Sole Proprietorship | One | Yes | Yes | Yes | Personal/ Passthrough |

| Partnership | Unlimited | Yes * | Yes | Yes | Personal/ Passthrough |

| C Corp | Unlimited | No | No (but they may) | No | Double |

| Limited Partnership | Unlimited** | GP - Yes LP - No | GP - Yes LP - No | GP - Yes LP - No | Personal/ Passthrough |

| LLC | Unlimited | No | Yes | No*** | Personal/ Passthrough |

| S Corp | At most 100 | No | No (but they may) | No | Personal/ Passthrough |

* Each partner is liable for full amount.

** At least one general partner (GP). No limit on limited partners (LPs).

*** However, most LLCs require the approval of the other members to transfer your ownership.

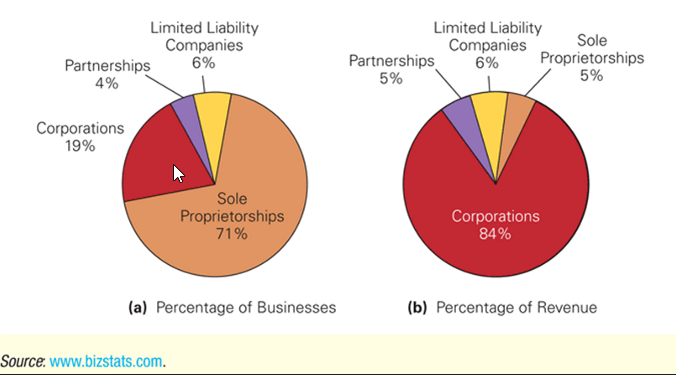

Shareholders in S corporations must be individuals who are U.S. citizens or residents [so they actually pay US income tax], and there can be no more than 100 of them. Because most corporations have no restrictions on who owns their shares or the number of shareholders, they cannot qualify for subchapter S treatment. Thus most large corporations are“C” corporations, which are corporations subject to corporate taxes. S corporations account for less than one quarter of all corporate revenue.

Sole Proprietorship

- Business owned and operated by one person

- Straightforward and many new businesses use this organizational form

- Principal limitation is that there is no separation between the firm and the owner

- The firm can have only one owner

- The owner has unlimited personal liability for any of the firm’s debts

- The life of a sole proprietorship is limited to the life of the owner

- It is difficult to transfer ownership of a sole proprietorship

Partnership

- More than one owner

- All partners are liable for the firm’s debt

- A lender can require any partner to repay all the firm’s outstanding debts

- The partnership ends on the death or withdrawal of any single partner

- Partners can avoid liquidation if the partnership agreement provides for alternatives such as a buyout of a deceased or withdrawn partner

Limited Partnership

A limited partnership is a partnership with two kinds of owners, general partners and limited partners

General partners

- Have the same rights and privileges as partners in any general partnership

- Are personally liable for the firm’s debt obligations

Limited partners

- Have limited liability and their ownership interest is transferable

- They have no management authority

Limited Liability Companies (LLC)

- Like a limited partnership but with no general partner

- All the owners have limited liability, but they can also run the business

Corporation

A corporation is a legally defined, artificial being, separate from its owners (“corpor” means body, so it’s a firm that has its own body, legally speaking)

- It has many of the legal powers that people have

- It can enter into contracts, acquire assets, incur obligations, and it enjoys protection under the U.S. Constitution against the seizure of its property

- A corporation is solely responsible for its own obligations

- The owners of a corporation are not liable for any obligations the corporation enters into

- The corporation is not liable for any personal obligations of its owners

Formation of a Corporation

- Must be legally formed

- Must be chartered in the state in which it is incorporated

- Corporate charter specifies the initial rules that govern how the corporation is run

- More costly than setting up a sole proprietorship

- The entire ownership stake of a corporation is divided into shares known as stock

- The collection of all the outstanding shares of a corporation is known as the equity of the corporation

Ownership of a Corporation

- An owner of a share of stock in the corporation

is known as a shareholder, stockholder, or

equity holder - Shareholders are entitled to dividend payments

- Usually receive a share of the dividend payments that is proportional to the amount of stock they own

- No limitation on who can own its stock

Tax Implications for Corporations

C Corporations

- Most corporations are C corporations.

- Must pay corporate taxes on its profits.

- Since individuals must pay personal income taxes on these dividends, shareholders in a C corporation effectively must pay taxes twice

- A C corporation’s profits are subject to taxation separate from its owners’ tax obligations

- Shareholders of a corporation effectively pay taxes twice

- The C corporation pays tax on its profits

- When the remaining profits are distributed to the shareholders, the shareholders pay their own personal income tax on this income

✏️ You are a shareholder in a C corporation. The corporation earns $5 per share before taxes. After it has paid taxes, it will distribute the rest of its earnings to you as a dividend. You will pay taxes on this dividend. The corporate tax rate is 40% and your tax rate on dividend income is 15%. How much of the earnings remains after all taxes are paid? What is your effective tax rate?

✔ Earnings Before Taxes = $5, Corporate Tax Rate = 40%

Taxation #1: Post-Tax Earnings (Net Income) = $5*(1-40%) = $3

The $3 of earnings are distributed as dividends, on which you pay a 15% dividend income tax.

Taxation #2: Your after-tax take = $3 * (1-15%) = $2.55

A total of $5-$2.55=$2.45 of taxes has been paid. This is $2.45/$5=49% of the initial earnings before taxes, so your effective tax rate is 49%.

S Corporations

- The firm’s profits/losses are not subject to corporate taxes. The taxes are “pass-through,” much like a partnership.

- Instead profits/losses are allocated directly to shareholders based on their ownership share

- Shareholders must include these profits as income on their individual tax returns, even if no money is distributed to them

✏️ Rework the C Corporation example assuming the corporation in that example has elected subchapter S treatment and your tax rate on non-dividend income is 30%.

✔ All of the income is treated as personal income and taxed at the 30% rate. Taxes = $5*30% = $1.5 After tax earnings = $5*(1-30%) = $3.5

Note: However, note that in a C corporation, you are only taxed when you receive the income as a dividend, whereas in an S corporation, you pay taxes on the income immediately regardless of whether the corporation distributes it as a dividend or reinvests it in the company.

Distribution of firm types in the US

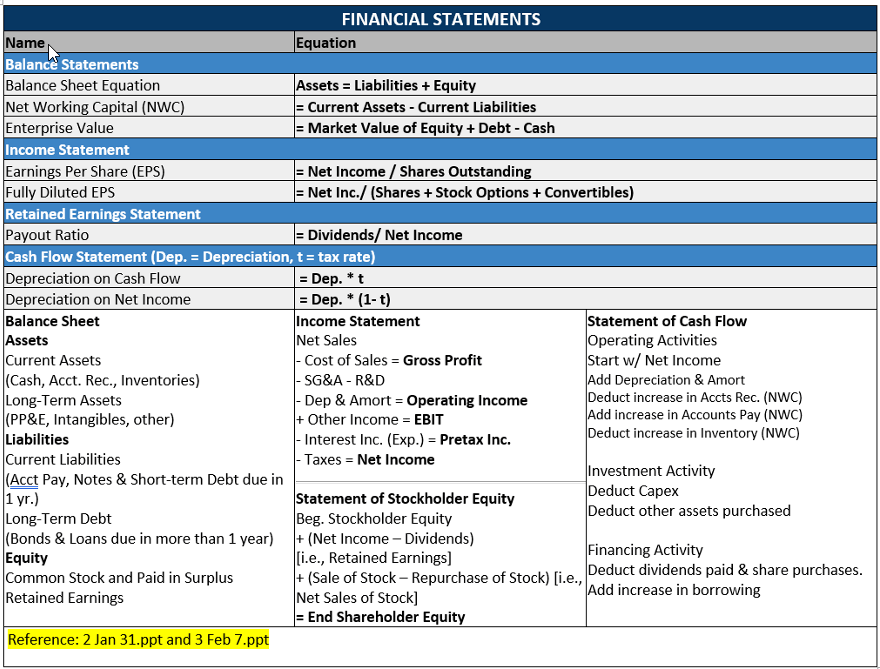

The Balance Sheet

- Also called “Statement of Financial Position”

- Lists the firm’s assets and liabilities

- Provides a snapshot of the firm’s financial position at a given point in time

The Balance Sheet Identity

- The two sides of the balance sheet must balance

Balance Sheet: Assets

Current Assets

- Cash and other marketable securities

- Short-term, low-risk investments

- Easily sold and converted to cash

- Accounts receivable

- Amounts owed to the firm by customers who have purchased on credit

- Inventories

- Raw materials, work-in-progress and finished goods;

- Other current assets

- Includes items such as prepaid expenses

Long-Term Assets

- Assets that produce benefits for more than one year

- Reduced through a yearly deduction called depreciation according to a schedule that depends on an asset’s life

- Depreciation is not an actual cash expense, but a way of recognizing that fixed assets wear out and become less valuable as they get older

- The book value of an asset is its acquisition cost less its accumulated depreciation

- Other long-term assets can include such items as property not used in business operations, start-up costs in connection with a new business, trademarks and patents, and property held for sale

Balance Sheet: Liabilities

Current Liabilities

- Accounts payable

- The amounts owed to suppliers purchases made on credit

- Notes payable and short-term debt

- Loans that must be repaid in the next year

- Repayment of long-term debt that will occur within the next year

- Accrual items

- Items such as salary or taxes that are owed but have not yet been paid, and deferred or unearned revenue

Long-Term Liabilities

- Long-term debt

- A loan or debt obligation maturing in more than a year

Net working capital

The capital available in the short term to run the business: Net Working Capital = Current Assets - Current Liabilities

The main components of net working capital are cash, inventory, Accounts Receivable, and Accounts Payable, so, particularly when covering incremental Free Cash Flows, we often write: Net Working Capital = Cash + Inventory + AccountsReceivable - AccountsPayable From this it follows that: ΔNWC = ΔCash + ΔInventory + ΔAR - ΔAP Don’t forget that NWC is subtracted when calculating Free Cash: Cash Effect of a change in NWC = -ΔNWC

* Note that when we calculate incremental Free Cash Flows we do not include short-term financing such as notes payable or short-term debt because those represent financing decisions that we keep separate from our investment decisions.

Stockholders’ Equity

Market Value Versus Book Value

- Market Value = Market capitalization

- Market Cap = Market price per share times number of shares outstanding

- Does not depend on historical cost of assets

- Book value of equity

- Net worth from an accounting perspective

- Assets - Liabilities = Equity

- True value of assets may be different from book value

Also called Price-to-Book ratio Sometimes used to classify firms as value (low M/B) or growth (high M/B)

Enterprise Value

The value of the underlying business assets, unencumbered by debt and separate from any cash and marketable securities

Enterprise Value = Market Value of Equity + Debt - Cash

See: 🔎 What is Enterprise Value?

✏️ The following represents Heinze in 2013.What is Market Cap and Enterprise Value?

| Share Price | $72.36 |

|---|---|

| Shares outstanding | 320.7 million |

| Cash | $1.10 billion |

| Debt (book) | $4.98 billion |

✔ Click here to view answer

Market Cap = Share Price * Shares Outstanding = $72.36 * 320.7 = $23,205.85 =$23.21 Billion

Enterprise Value = Market Value of Equity + Debt - Cash = $23.21 Billion + $4.98 billion - $1.10 billion = $27.09 billion.

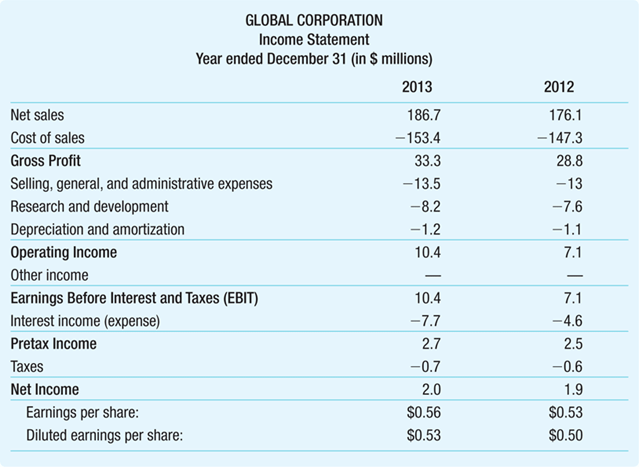

Income Statement

The income statement lists the firm’s revenues and expenses over a period of time

- Sometimes called the profit and loss statement, or “P&L” The last or “bottom” line of the income statement shows net income

- A measure of its profitability during the period

- Also referred to as the firm’s earnings

Earnings Calculations

- Revenue (top line)

- Gross Profit

- Revenues (Net Sales) - Cost of Sales = Gross Profit

- Operating Expenses

- Gross Profit - Operating Expenses = Operating Income

- Earnings Before Interest and Taxes (EBIT)

- Operating Income +/- Other Income = Earnings Before Interest and Taxes

- Pretax and Net Income

- EBIT +/- Interest income (Expense) = Pretax Income

- Pretax Income - Taxes = Net Income

Earnings Per Share = Net income reported on a per-share basis

Fully diluted EPS increases number of shares by:

- Stock options issued to employees

- The right to buy a certain number of shares by a specific date at a specific price

- Shares issued due to conversion of convertible bonds

- Convertible bonds are corporate bonds with a provision that gives the bondholder an option to convert each bond into a fixed number of shares of common stock

EBITDA

- Financial analysts often compute a firm’s earnings before interest, taxes, depreciation, and amortization, or EBITDA

- Because depreciation and amortization are not cash flows, this subtotal reflects the cash a firm has earned from operations